Make A

Difference

July 28–August 3

Gift period-care products

for a teenage girl in need.

Imagine opening an investment account for your child and starting with $1,000 already deposited to help them build long-term financial security from day one. That’s the idea behind Trump Accounts, a new federally-backed program designed to help American children under 18 start building a stronger financial foundation early in life.

A strong start matters—financially, emotionally, and in every way that shapes a child’s future.

Trump Accounts are federally sponsored investment accounts created to help American children under 18 build long-term financial security. Think of them as a future-focused savings tool with an investing component—something families can add to over time, with the goal of giving kids a stronger foundation as they grow. Parents can contribute, and in some cases, employers may be able to contribute, offering another way to build momentum for a child’s future.

The program was introduced through the One Big Beautiful Bill Act, signed into law in July 2025. Under the original legislation, newborns can receive a one-time $1,000 seed contribution from the U.S. Treasury to start their account if they are eligible under the regulations. These accounts are currently designed to be live by July, 2026, but you can begin to take actions to sign up now.

In early December 2025, philanthropists Michael and Susan Dell pledged $6.25 billion to help expand the program—funding an additional $250 contribution per child for millions of children based upon specific eligibility criteria that are being established by the Dells.

Then on December 17, 2025, billionaire investor Ray Dalio (founder of Bridgewater Associates) and his wife Barbara announced a similar pledge for eligible children in Connecticut—committing $250 per child for children under 10 in Connecticut ZIP codes where the median household income is under $150,000.

Inspired by these gifts, Treasury Secretary Scott Bessent announced a “50 State Challenge”—an effort to encourage philanthropists across the country to step in and help seed more children’s accounts state by state.

Here’s the encouraging part: under current regulations, any child under 18 can have a Trump Account opened for them. The bigger question most parents are asking is whether their child qualifies for the free seed money that helps jumpstart the account.

When Trump Accounts were first introduced, the government’s seed deposit was specifically tied to certain birth years. Below is the simplest way to break it down under the regulations as of February 1, 2026:

Your child qualifies for the full $1,000 federal contribution if they:

Were born between January 1, 2025 and December 31, 2028

Are a U.S. citizen

Have a Social Security number

And here’s a relief for many families: this $1,000 deposit does not require an income minimum or income cap.

Even if your child is not eligible for the seed deposit, there are still great reasons for opening a Trump Account. Private businesses and individuals are helping to fill the gap with additional resources that can help. And, even without the seed funds, there are potential advantages for Trump Accounts that you should discuss with your trusted financial professional.

Once your child’s Trump Account is opened, it’s designed to grow with them over time. Instead of functioning like a typical piggy bank, a Trump Account works more like a long-term investment account—meaning the money inside can grow year after year with the goal of building a stronger financial foundation for adulthood.

Parents can add to the account over time. In some cases employers and approved organizations may be able to contribute too. The big idea is simple: give families the opportunity to start early—even with small amounts—and let time do the heavy lifting.

Trump Accounts are built to allow parents to keep it simple and flexible. According to White House program materials and current regulations:

Trump Accounts are meant to be long-term, so kids generally won’t be pulling money out during childhood.

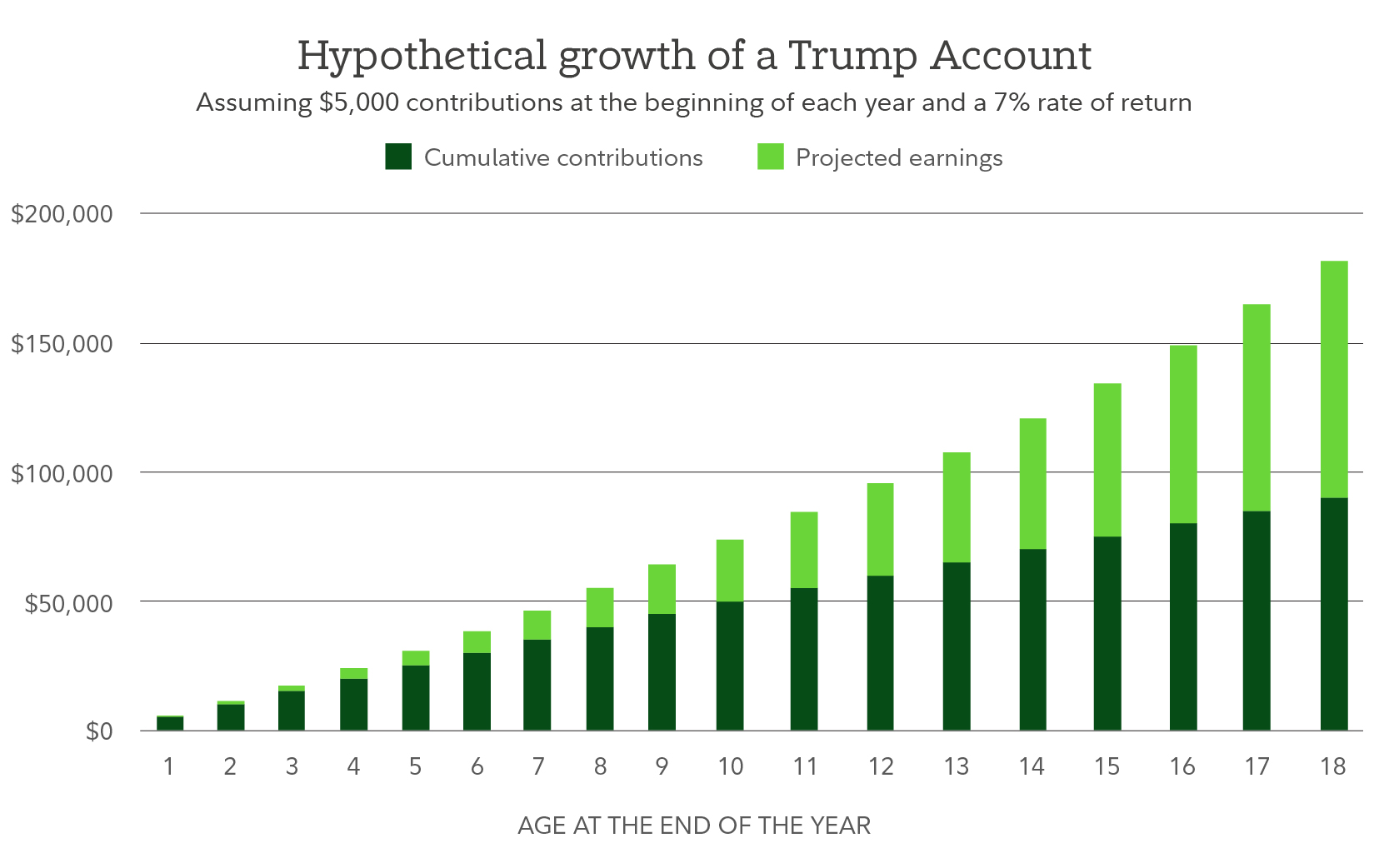

In other words: this isn’t meant to be “quick cash.” It’s built for bigger future moments. As this chart from Fidelity shows, consistent contributions can yield significant returns:

The program is currently designed to support major life milestones—things that help young adults build stability as they step into adulthood.

Under current rules, qualified uses may include:

These guardrails are meant to keep the account focused on building a future—not just spending.

Opening a Trump Account is designed to be simple—even if you’re not a “finance person.” The key thing to know is that enrollment happens through the IRS, and it’s tied to a new form created specifically for this program, as well as resources from the Trump administration (centralized at www.trumpaccounts.gov).

Here’s what parents can expect as the rollout continues.

Trump accounts are just one of many options when planning for your child's future and their future needs. To help you decide what is best for your specific circumstances, you should speak with an investment advisor before making any decision or investment.

Here are a few parent-friendly reminders to keep expectations grounded and hope realistic:

Have Additional Questions?

There are fantastic resources available from the following sources:

https://trumpaccounts.gov

https://www.irs.gov/newsroom/treasury-irs-issue-guidance-on-trump-accounts-established-under-the-working-families-tax-cuts-notice-announces-upcoming-regulations

https://home.treasury.gov/news/press-releases/sb0372

https://www.fidelity.com/learning-center/personal-finance/trump-accounts

https://www.schwab.com/learn/story/trump-accounts

(Above) Quick Comparison of Savings Accounts for Minors